Podcasts

Watch videos featuring supply chain experts

In 2024, U.S. customs officials flagged more than $38 billion in trade as potential sanctions violations, and yes, a lot of it came from importers who honestly had no idea their own supply chain brushed up against a restricted entity. That whole visibility gap, it’s getting hard to ignore, especially for modern enterprises because global commerce isn’t just about managing transportation anymore, it’s also about threading through a kind of constantly shifting regulatory minefield. With Washington using trade policy more and more as a national security tool, “compliance” has slipped out of the back office and into the boardroom. Importers can’t afford to look only at their immediate suppliers; they need to map every layer of the supply chain, not as a nice-to-have but as a defence against sudden enforcement actions, multi-million-dollar penalties, and those brutal border seizures.

Derivative Tariff: A duty applied to downstream, finished, or semi-finished products that contain primary raw materials already subject to trade restrictions, even if the final imported product falls under an entirely different trade classification.

When a government levies heavy tariffs on a raw material like raw steel, or aluminium, foreign manufacturers quite often adapt by processing those metals locally into finished goods, for example automotive parts, steel bolts, or even metal furniture. They then ship those items outward instead. In practice, this kind of behaviour sort of jumps around the first trade barrier. A derivative tariff can be used as an anti-circumvention instrument, meaning it pushes the tax along to the downstream goods too, so foreign producers can’t bypass the original trade protection just by moving the manufacturing process ahead one or two steps, like rearranging the whole value chain a bit.

In the United States, the main legal lever behind these moves is Section 232 of the Trade Expansion Act of 1962. Basically, this law gives the U.S. President the power to put tariffs on or set import quotas, without getting Congress involved first, as long as the Department of Commerce finds that a product is coming in “in such quantities or under such circumstances as to threaten or impair national security.”

Expanded Product Scope: Section 232 duties now heavily penalize downstream derivative products. These tariffs are primarily applied on HS Chapter 73 (articles of iron or steel) and HS Chapter 76 (aluminium articles), but also span numerous other chapters like 82, 84, 85, and 94 for finished goods containing these metals. This covers a massive $151 billion trade base, capturing everything from auto body panels and air conditioning parts to metal office furniture and consumer sports gear.

The Sourcing Transparency Crackdown: Importers must trace materials back to their absolute origin. Customs strictly enforces strict reporting mandates, such as the Country of Melt and Pour for steel and the Country of Smelt and Cast for aluminium. Failing to properly identify or verify where the raw metal was originally melted can trigger default penalty tariffs as high as 200%.

When corporate leadership evaluates exposure to new trade policies, they almost exclusively look at the headline percentage figure the tariff rate. If a rate drops from 50% to 25%, a standard financial forecasting model assumes a 50% reduction in duty liability.

However, a tariff is always a product of two variables:

Total Duty Owed =Tariff Rate × Valuation Bas

The Nominal Rate Illusion occurs when an organization celebrates a reduction in the Rate while completely overlooking an aggressive, structural expansion of the Valuation Base. Under the modern Section 232 framework enacted via recent Presidential Proclamations, U.S. Customs and Border Protection (CBP) fundamentally changed the definition of that valuation base for derivative products.

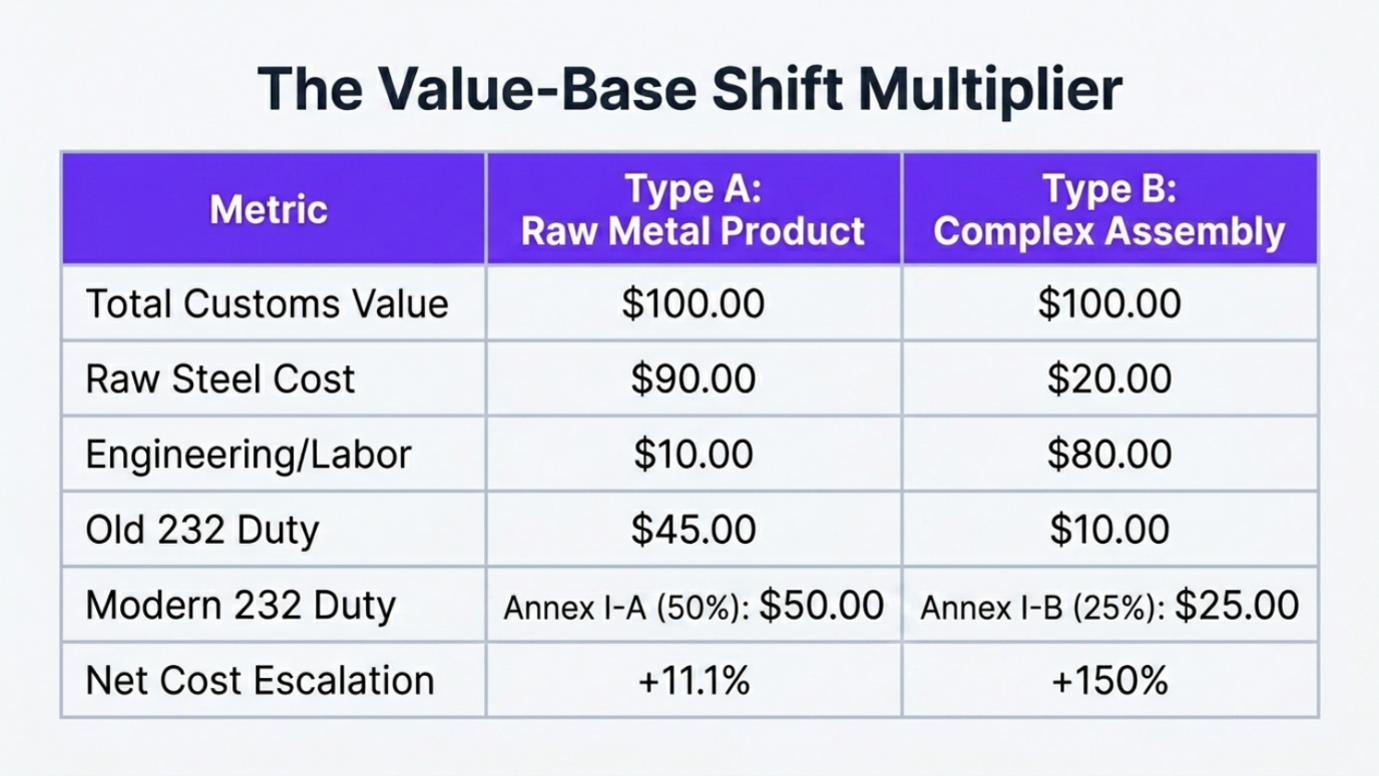

Historically, Section 232 tariffs on derivative goods operated using a kind of bifurcated “split-line” reporting method. In practice, it tried to isolate the target metal (the perceived national security threat) from the rest of the product assembly. So, if a company imported a complex industrial item, like an electronic actuator that includes internal steel brackets or a specialized heavy duty valve, CBP would require the importer to work out the separate, stand-alone value of the raw metal content sitting inside it.

Deductive approach: importers often leaned on Bills of Materials (BOMs) plus mill test certificates to figure the transaction value of the raw steel sheet or aluminium coil used right at the very start of production.

Excluded overhead: all downstream foreign value adds, including precision machining, stamping, structural assembly, engineering labour, surface coating, and even foreign factory profit margins, were legally carved out and kept away from the 232 calculations.

The arithmetic: Let us assume that custom value of a product is $100. Even if the rate was extremely punitive, say 50%, the valuation base stayed constrained to that raw $20 metal core alone.

Duty Owed = 50%×$20 = $10.00

The modern regulatory framework mostly, but not exactly, abolished this content-based isolation model. To streamline border administration and aggressively eliminate some loopholes, CBP pivoted to a classification driven methodology, kind of as if the system needed to “know” the right bucket first. So, now if a derivative product lands under an HTS code that’s captured by the Section 232 annexes, like Annex I-B, then the tariff rate is applied directly onto the Full Entered Customs Value for the entire line item.

Duty Owed= 25%×$100 = $25.00

The new Section 232 derivative framework sort of breaks trade enforcement into two main lanes, mostly based on how complicated the product really is. Annex I-A goes after primary raw metals and other simple, low-margin wares (for instance cast iron pipes or structural blocks). Since these items are basically raw material, they get stuck with a higher starting point, a 50% tariff rate that’s applied to the whole entered customs value, no real deductions. Explain On the other hand, Annex I-B is aimed at downstream, tightly engineered finished assemblies (like precision actuator valves or industrial fasteners). To avoid major supply chain headaches, Annex I-B keeps a lower 25% nominal tariff rate. Still, the catch is that this percentage lands on the entire transaction value, including foreign labour, R&D, and engineering overhead. So, Annex I-B imports often end up causing a larger net financial duty jolt for corporate importers.

To prevent your procurement teams from falling victim to this illusion, you can establish an ironclad mathematical threshold to identify which products are at risk. The tipping point where the modern 25% full-value tariff equals the old 50% content-only tariff can be found using a simple ratio: Let assume that the duties paid in old and new duty are the same.

Old Duty=New Duty

50%×Metal Value=25%×Full Value

(Metal Value) / (Full Value) = (25% / 50%) = 50%

Strategic Takeaway: If a product requires precision machining, heavy fabrication, or multi-step assembly, those non-metal costs are now fully tariffed at the border under Section 232 derivative rules.

To mitigate these costs, supply chain teams must execute on specific regulatory exclusions:

Lever 1: The 15% De Minimis Weight Exemption

The 15% De Minimis Weight Exemption serves as an absolute statutory carve-out designed to protect mixed-material assemblies from punitive trade penalties.

The Legal Threshold: Under HTS provision 9903.82.03, finished articles listed in the derivative annexes are subject to a 0% Section 232 ad valorem duty rate, provided the aggregate weight of the covered metals (steel, aluminium, or copper) accounts for less than 15% of the total imported article's weight.

The Restriction Ceiling: this exemption is strictly barred for any goods that are basically classified under HTS Chapters 72, 73, 74, or 76, (which pretty much govern primary metals and baseline metal articles). It’s meant for downstream sectors, like multi-material automotive subassemblies, intricate electronics housings, consumer appliances, or medical device casings, where the components are mixed up and the overall setup gets handled differently.

Lever 2: The "Circular Sourcing" Pivot (10% Preferential Rate)

The modern framework gives businesses a bit of a strange but clear nudge to lean on domestic upstream supply chains, even when the final downstream manufacturing ends up happening overseas.

So how it works : when you bring in foreign-made derivative items that would normally get hit with a 25% or 50% penalty tariff , you may be allowed to use a simpler 10% flat ad valorem duty, but only if the importer can show that at least 95% of the base metal was originally melted and poured (for steel) or smelted and cast (for aluminium and copper) somewhere inside the United States.

The Compliance Hurdle: This lever eliminates the previous rule where any trace of U.S. metal granted a total exclusion. Importers must now maintain ironclad, un-broken trace documentation. A failure to provide mill test certificates verifying the 95% threshold defaults the shipment to the maximum penalty rate.

Lever 3: Preferential Ally Corridors (The United Kingdom Framework) To insulate global supply chains from single-source disruptions, corporations must actively map their vendor footprints against country-specific strategic exemptions. The Framework Mechanics: Importers can exploit specific bilateral agreements that slash baseline derivative duties. For example, under the U.S.-UK trade arrangements, qualified derivative imports see a major structural markdown:

o Annex I-A Goods: Compressed from a 50% rate down to 25%

o Annex I-B Goods: Compressed from a 25% rate down to 15%.

The origin trap, for getting these preferential tiers, is basically this: the importer has to show that, at minimum 95% of the metal was melted and poured, or smelted and cast, right there within the United Kingdom. If they’re buying supply from a UK fabricator who depends on primary metal billets coming from non-market economies then the whole entitlement falls apart, like it doesn’t hold up, and it will set off full enforcement action.

The transition from a content-based raw material tax to a classification driven tariff on the Full Entered Customs Value alters more than just product margins. It triggers a cascading set of disruptions across an enterprise's financial statements. When a derivative product falls under Section 232 Annex architectures, the financial penalty impacts the balance sheet, pushes cash outlays earlier in the operational cycle, and creates hidden liabilities.

Balance Sheet & Working Capital Distortions

The immediate effect of full-value derivative tariffs looks like a severe, kind of sudden widening of working capital needs, mostly because there are two main balance sheet entries that get pulled along, even if people focus elsewhere. It’s not just a minor hiccup either.

Inventory Valuation (Asset Inflation): Under normal reporting rules, like US GAAP and IFRS, landed costs, including import duties, have to be folded into the inventory cost. So, since the tariff is charged on the entire engineered assembly value not only the raw metal portion the capitalized inventory number gets pushed up. That means the cash outflow turns into a bigger asset first, and the expense stays off the Income Statement until the item is actually sold. Even so, it “inflates” current assets in an artificial way, and that part is what really matters.

Accounts Payable & Cash Drifts: Meanwhile, to keep raw material flows steady, the firm has to put up a lot more upfront cash to clear customs brokers and port authorities. That causes a structural mismatch too, current assets rise because of those heavier inventory numbers, but cash drops fast, which in turn stretches the Cash Conversion Cycle (CCC) longer than before.

Cash Flow Statement: Operating vs. Financing Liquidity

The “Full-Value Capture” thing shifts cash outflows a bit sooner in the supply chain rhythm, so it ends up tugging liquidity right away. You see it as an almost immediate drag: Operating Cash Flow, CFO Drain, that part happens because tariff outlays show up as cash outflows inside operating activities. So when a company gets hit by a 150% duty jump on finished components, the net cash coming from operating activities dips basically right then. And that means there’s less cash around to cover day to day operations, keep funding for research and development, or handle short term debt obligations, without stress.

Then there’s the Escrow & Customs Bond Freeze part. To keep goods flowing through ports while they’re under strict Section 232 scrutiny, companies are frequently told by customs authorities to raise the value of their Continuous Customs Bonds. In practice, corporate treasuries have to post support either direct cash payments, or through restricted bank letters of credit back to the bonding companies. This effectively pulls liquid cash out of active operations and tucks it into longer-term Restricted Cash accounts, so capital gets locked away and can’t earn a return like it otherwise would.

When customs authorities switch enforcement to full entered customs value, the risk is no longer just a line-item expense on a profit-and-loss statement, it becomes an immediate liquidity crisis for the corporate treasury. Because full-value assessments exponentially inflate the total dollar amount collected at the border, U.S. Customs and Border Protection (CBP) has dramatically ramped up its automated post-summary audit procedures.

Under modern enforcement rules, a shipment can clear the port seamlessly today, only for the importer to receive an official CBP Form 28 (Request for Information) months later demanding unbroken documentation for "Melt and Pour" origin tracking. If the company cannot produce this data within the strict statutory window, CBP can retroactively liquidate those past entries at a 200% default penalty rate.

This creates two massive macro-financial risks:

From a macro corporate treasury angle, an enterprise Global Trade Management (GTM) platform works less like an administrative tool and more like an automated financial risk hedge. It keeps on validating and storing very solid digital records like mill test certificates and country-of-smelt declarations at the same exact moment a transaction happens. So, the overall GTM setup ends up building this defensive, audit-ready data fortress. Then, if a retroactive sovereign audit, or a lookback inquiry gets triggered, the platform can instantly bring in the required trace documentation. That fast resolution removes the chance of default penalty escalations, reduces corporate customs bond premiums in a pretty dramatic way, and it also releases critical working capital that would otherwise get tied up because of regulatory uncertainty.

Traditional corporate structures isolate the trade compliance department from upstream procurement and R&D design workflows. In a regulatory climate where minor design choices such as a component weighing 14.5% metal versus 15.5% metal, dictate whether an item faces a 0% de minimis rate or a 25% full-value tariff, this isolation is unsustainable. Sourcing decisions can no longer be based purely on ex-works pricing and localized labour arbitrage.

Modern global trade platforms break down these operational silos by embedding real-time, cross-border macro intelligence directly into corporate financial modelling. By linking algorithmic landed-cost engines with global trade databases, GTM ecosystems serve as a predictive analytics foundation for executive decision-makers. It enables engineering and procurement teams to run simulated scenarios on alternative sourcing corridors (such as tracking preferential ally pathways or verifying U.S.-origin metal content thresholds). This elevates global trade compliance from a routine back-office cost center to a core asset that actively guides corporate tax strategy, supply chain reshoring, and long-term capital allocation.